Many people don’t realize they need to report class action settlement money to the IRS until a tax form arrives months later or their accountant asks questions they weren’t prepared for.

Reporting settlement income is rarely as straightforward as entering a single value on your tax return. The reporting process can change depending on whether the payment involved wages, business income, attorney fees, interest, or multiple types of damages within the same settlement.

This guide explains how to report settlement payments on a tax return, which IRS documents you may receive, and where settlement income is typically reported on Form 1040. You’ll also learn about the common filing mistakes that can lead to penalties, audits, or overpaying taxes, and how to avoid them.

Is settlement money considered income?

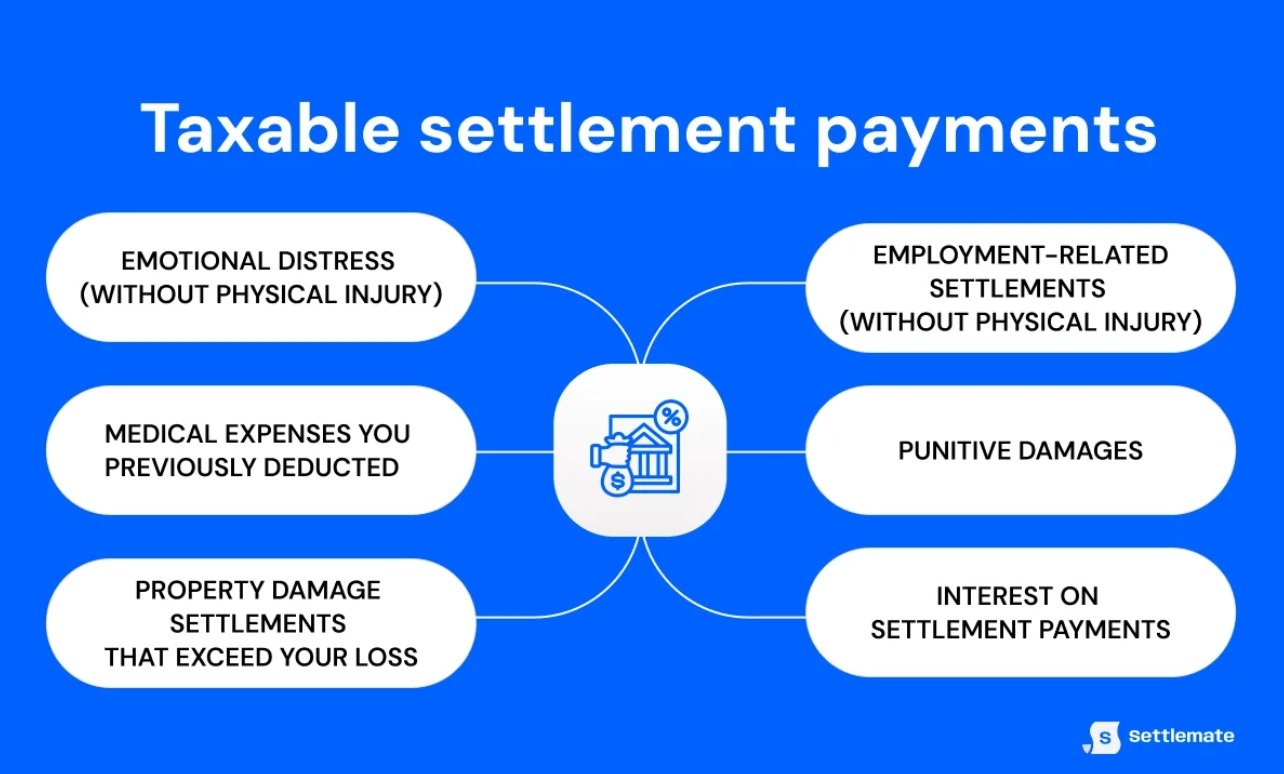

Settlement money can be considered taxable income by the IRS. Tax treatment of settlement payments depends on the specific damages they were intended to replace.

Some settlements are taxable, while others can be fully or partially non-taxable. Here’s a quick overview:

In some cases, a single settlement can include both taxable and non-taxable portions. For instance, a class action lawsuit may include compensation for physical injuries alongside punitive damages or interest.

The IRS looks beyond the final payment. How the settlement should be reported on your tax return depends on factors such as:

- How the settlement was categorized

- Whether taxes were withheld

- How attorney fees were handled

- How the payment was structured

That’s why settlement payments are often accompanied by tax forms, which help determine how to report these funds on your tax return.

What tax forms for the settlement payment may you receive?

Different settlement payments are reported on various IRS forms depending on the type of claim and the category of the payment.

Here’s an overview of common settlement tax forms and when they’re used:

Good to know: Even if an underlying settlement is tax-free, any accrued interest is always taxable. A settlement may also contain several payment categories, in which case you may receive multiple forms. An appropriate example of this is an employment settlement with wages and additional damages.

Who sends tax forms for settlement payments?

In a settlement, tax forms are usually issued by the party that makes or processes settlement payments. You don’t typically request these forms yourself, and they don’t come directly from the IRS. They’re part of the IRS third-party reporting system used to track taxable income.

More specifically, tax forms may come from:

- The defendant: Usually responsible for reporting settlement payments, especially when a settlement includes taxable components like lost wages or punitive damages

- An insurance company: Often issues tax forms if they fund settlement payments on behalf of the defendant, especially in personal injury claims, employment disputes, liability settlements, or property damage cases

- An employer: Responsible for issuing tax forms in employer-related settlements, such as those involving severance, back pay, or wrongful termination

- A law firm: Typically issues tax forms related to the settlement process, particularly for attorney fees or payments made to experts, consultants, or service providers

How to report settlement fund money on tax returns

You typically don’t report class action settlement money on your tax return as a single lump sum entry. You need to break it into categories like wages, damages, or interest, all of which require a different form.

While you may need to consult a tax professional for complex and high-value settlements, paying taxes on a settlement usually involves three core steps:

- Reviewing your settlement agreement

- Reconciling your tax forms with settlement reporting

- Accounting for lawyer fees

1. Reviewing your settlement agreement

You must identify how the payment is allocated in the settlement agreement. The IRS generally respects clear allocations between different types of damages (e.g., wages vs. emotional distress vs. medical costs), as long as they’re consistent with the underlying claim.

If the agreement itemizes amounts, use the stated allocations to determine which portions are taxable. But if you’re only given a lump sum, you must allocate the settlement yourself based on the underlying claims.

Warning: The IRS can recharacterize allocations if they appear unsubstantiated or inconsistent with the case facts.

2. Reconciling your tax forms with settlement reporting

The type of tax forms you receive is critical because it dictates where on your tax return the amount must be reported. Each form corresponds to a different line or schedule on Form 1040.

Start by aligning the income type shown on your documents with the correct reporting category:

Some settlements require additional reporting beyond the standard forms.

For example, property damage settlements that fall below your adjusted basis are generally non-taxable. However, you must reduce your property’s cost basis by the settlement amount. If property-related settlements exceed your adjusted basis, the excess may count as taxable income and require reporting on Schedule D or Form 4797.

3. Accounting for lawyer fees

The IRS typically designates the full settlement amount, i.e., the amount before attorney fees are deducted, as your income. This means that even if your lawyer is paid directly from the settlement under a contingency fee agreement, you still need to report the gross amount on your tax return.

However, certain claims may allow an above-the-line deduction for attorney fees. This means you can deduct the legal fees directly from your income when calculating your taxable amount, which prevents taxation on money you never kept. These claims include:

- Employment discrimination

- Whistleblower awards

- Specific statutory claims

Outside of these exceptions, attorney fees don’t automatically reduce your taxable income. How the fees are treated depends on the type of claim and may require separate tax analysis to determine whether any partial deduction or alternative treatment applies.

Important: Always keep supporting documentation alongside your tax records, including settlement agreements, allocation breakdowns, tax forms, payment statements, and legal correspondence. The IRS recommends keeping tax records for at least 3 years, but you consider retaining them longer (7+ years) for complex settlements, amended returns, or audit risk situations.

Common mistakes when paying taxes on settlement money

Reporting settlement taxes might be complex, especially when the payment includes multiple categories of damages, attorney fees, or delayed payouts. Some of the most common mistakes to watch out for are:

- Reporting the wrong amount: You must report the gross settlement amount, not only the amount deposited into your bank account. This mistake usually happens when attorney fees are deducted before the payment is sent to you.

- Ignoring interest payments: Even when a portion of the settlement is non-taxable, interest added to the payout may need to be reported separately. People may overlook this portion because it may be on a separate tax form or added as a small line item within the settlement breakdown.

- Filing taxes before the settlement is paid: Class action lawsuits take time, and a settlement agreement may be signed months before the money is distributed. Tax reporting is based on when you or your attorney receives the funds, not when the case settles.

- Failing to keep settlement records and tax documents: You may encounter issues if the IRS questions the categorization of your settlement and you have not retained the appropriate paperwork.

But paying taxes on a settlement only becomes relevant if you actually get paid. Settlemate can help ensure that you claim all the class action settlements you’re entitled to.

Streamline your way to class action payments with Settlemate

To receive a settlement payment, you first need to file a claim. Many eligible claimants never get that far because they miss the notice, never realize they’re entitled to a payout, overlook the filing deadline, or never complete the claim process because it feels confusing and directionless.

Whatever the reason, the result is always the same: you leave money on the table.

Settlemate solves this problem with purpose-built automation. It simplifies the claim process by:

- Identifying eligible settlements based on your purchase history and emails

- Filling out claim forms whenever possible so you can submit directly through the app

- Keeping you updated on the progress of your claims, payout estimates, and deadlines

- Alerting you whenever a new eligible settlement appears

- Clarifying which documents you need to submit if a particular claim requires proof

- Tracking the claim status

Download Settlemate from the App Store or Google Play, set up your account, and start claiming the money that’s rightfully yours.

Settlemate’s refund policy makes sure that you make more money from the platform than you invest in it. If the savings you get in the first year don’t cover the cost of your subscription, you may be eligible for a full refund.

FAQs

What if you don’t receive a tax form for the settlement payment?

Not receiving a tax form doesn’t mean the settlement is non-taxable. The IRS may still expect you to report the taxable portions of the payment.

There are several reasons a form may be missing, such as:

- The payer isn’t legally required to issue a settlement tax form

- The payer mistakenly classified the payment as non-taxable

- The form was sent to an old address or was lost in the mail

If this happens, you should:

- Review your settlement agreement and payment breakdown to identify which portions are taxable under IRS rules

- Contact the payer or their attorney to request a form if you believe it should have been issued

- Report taxable settlement income on the appropriate line of your tax return, such as Schedule 1, line 8z for other income, or as wages on Line 1a if it has tax withholding

Can a settlement tax form be wrong?

Yes, settlement tax reporting mistakes happen. A payer may issue the wrong form, report the wrong amount, or fail to separate taxable and non-taxable portions correctly. Before filing your tax return, you must review:

- The settlement agreement

- The amount reported on the form

- Any allocations for medical expenses, wages, or interest

Why might you receive a tax form for a non-taxable settlement?

Receiving a tax form doesn’t automatically mean the entire settlement amount is taxable.

Sttlement payers sometimes issue forms broadly because failing to report a payment when required can trigger IRS penalties. As a result, some payers choose to report the payment even when a portion or the entire settlement may qualify for non-taxable treatment.